Episode Details

Back to Episodes

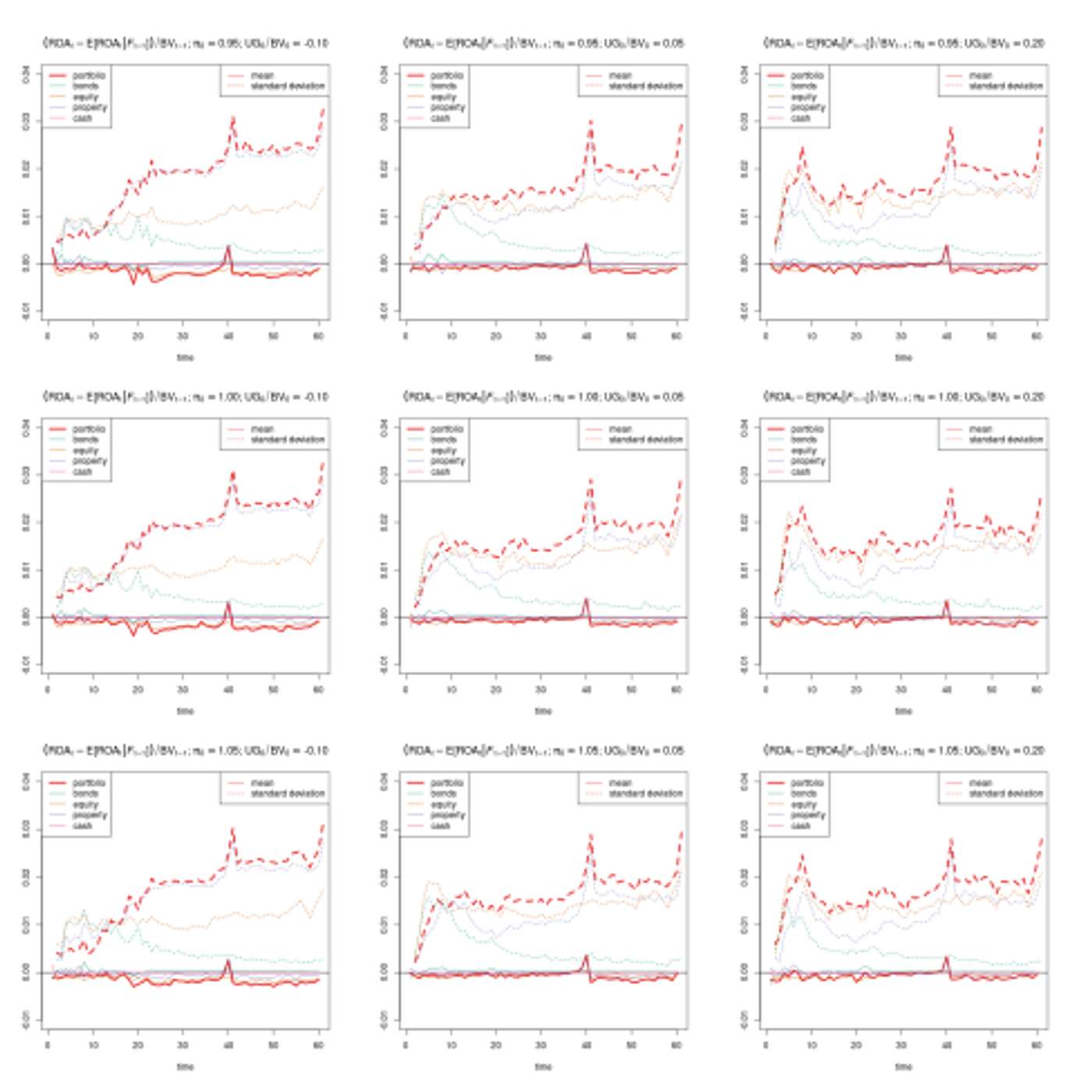

Estimating Future Discretionary Benefits Without Monte Carlo Simulation

Description

This story was originally published on HackerNoon at: https://hackernoon.com/estimating-future-discretionary-benefits-without-monte-carlo-simulation.

A deterministic framework for estimating future discretionary benefits in life insurance, offering tight bounds without Monte Carlo simulation.

Check more stories related to finance at: https://hackernoon.com/c/finance.

You can also check exclusive content about #insurance-regulation, #market-consistent-valuation, #solvency-ii, #actuarial-modeling, #mean-field-libor-market-model, #asset-liability-management, #monte-carlo-valuation, #financial-risk-modeling, and more.

This story was written by: @solvency. Learn more about this writer by checking @solvency's about page,

and for more stories, please visit hackernoon.com.

This article presents a deterministic method for estimating future discretionary benefits in life insurance portfolios by deriving stable upper and lower bounds, avoiding reliance on Monte Carlo simulations while maintaining market consistency.