Episode Details

Back to Episodes

If you invest in the wrong assets, you'll pay twice as much tax

Season 1

Episode 23

Published 8 years, 1 month ago

Description

The ultimate aim of investing is to build wealth. Current and future tax liabilities can have a significant impact on your ability to build wealth. Simply put, the less tax you pay, the more money you keep for yourself. Therefore, taxation is a major consideration.

That said, tax consequences should never drive investment decisions alone. Tax is one of many considerations so its important to not become too tax focused. Balance is the key here.

Income versus capital gainMost growth assets provide a combination of income and capital growth.

Income is taxed at your marginal tax rate (which is 39% for people earning between $87k and $180k p.a. or 47% if you earn more than $180k p.a.). However, only 50% of any realised capital gains are taxed at your marginal rate (because if you own the asset for more than 12 months you are entitled to reduce the net capital gain by 50%).

Therefore, capital gains attract half the tax than income does.

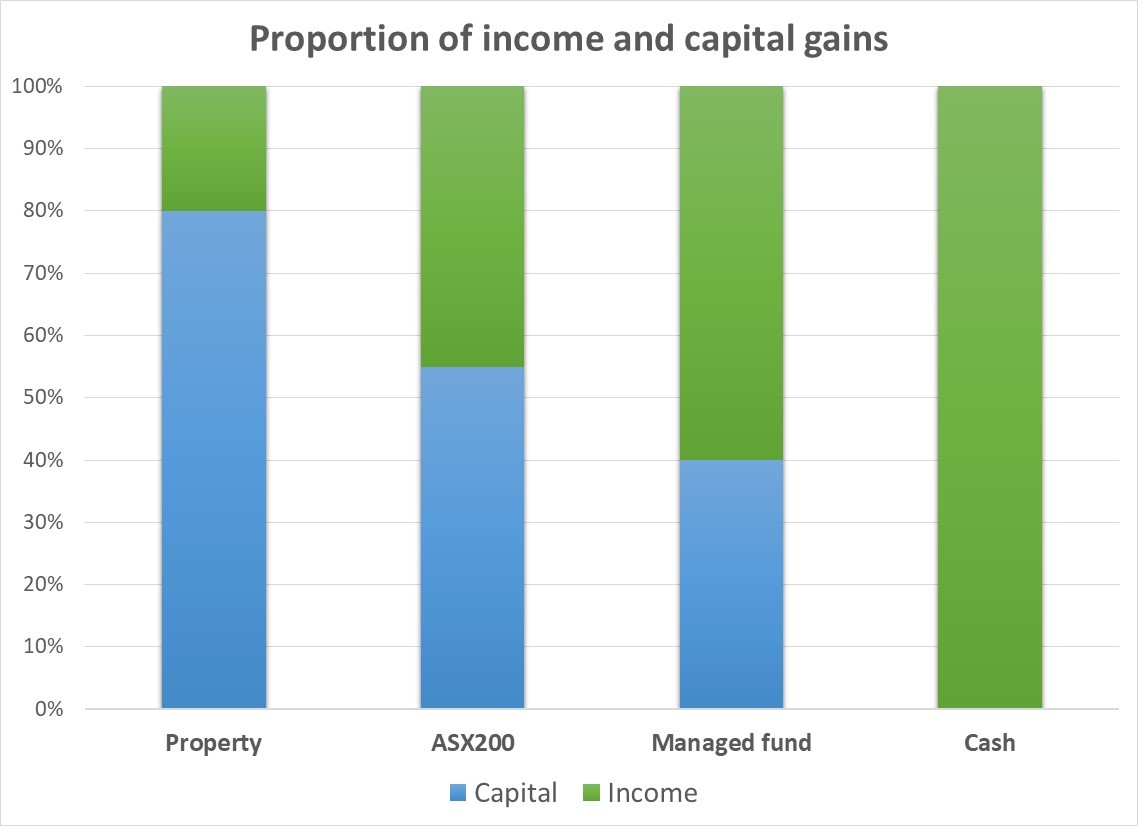

Compare asset classesThe chart below sets out the proportion of income and capital gains you can expect from investing in residential property, an index fund (ASX200), an actively managed fund and cash. Residential property provides most of its total return in capital growth and therefore is more tax efficient.

There are some other advantages of investing in assets that provide most of their return in capital (not income) including:

- You only pay capital gains tax when you sell the asset. However, income is taxed in the financial year it is received. This means that you get to reinvest the gross capital gain each year and avoid paying any tax until you sell it.

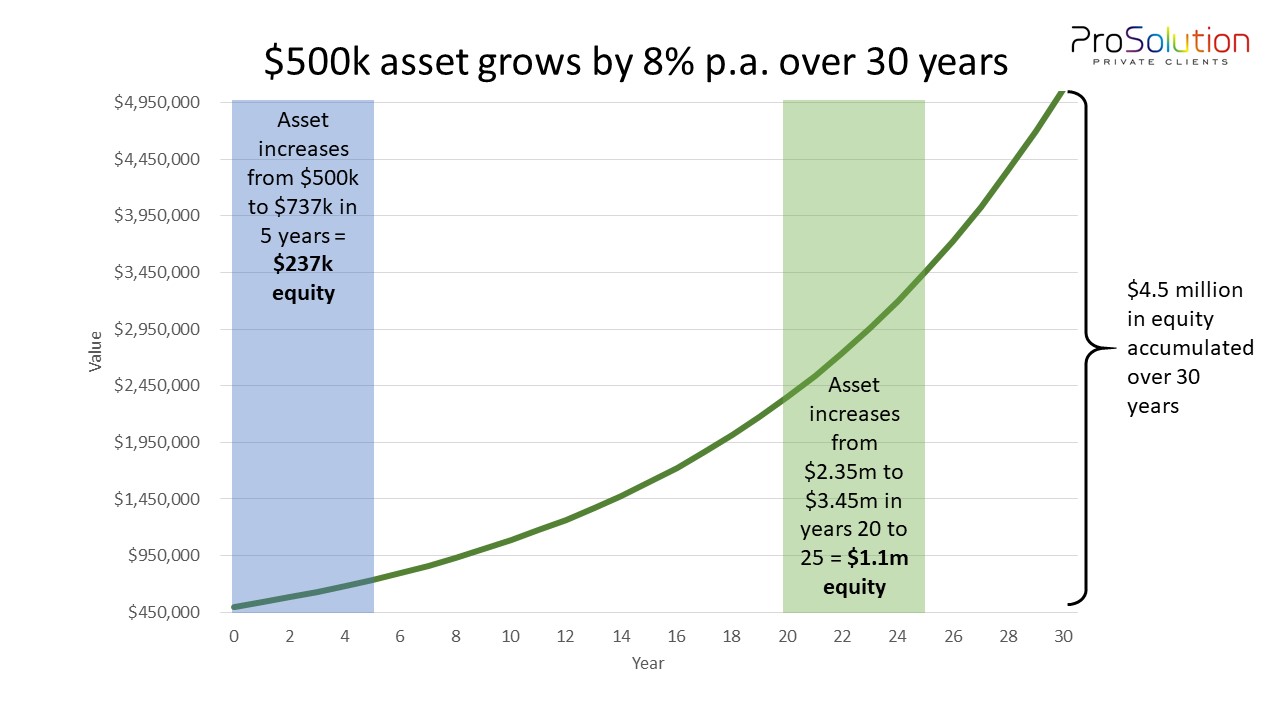

- This chart below demonstrates that you will enjoy more than four times more growth (in dollar terms) in the fifth 5-year period ($1.1m) comparted to the first 5-year period ($237k). This illustrates the power of compounding capital growth. Quality assets require time and patience. Its that simple.

Let’s compare income assets to assets that generate an overall return of 10 per cent pa each. The only difference between the two investments is the components of the return – one asset produces more income (and, therefore, less growth) than the other. As you can see from the following table, the investment that generates less income results in a lower tax expense and, therefore, a 1 per cent pa higher after-tax return. However, most importantly, the higher capital growth rate for asset two makes a massive difference on the value of the assets over the long run. Asset one is projected to be worth $1.45 million in 20 years, whereas asset two is projected to be worth $2.33 million – some $880,000 more. The point is, all things being equal, it’s very valuable to substitute less income in return for more capital growth.

Asset oneAsset twoIncome4.5%2.0%Capital growth5.5%8.0%Tax on income @ 40%(1.8%)(0.8%)After-tax total return8.2%9.2%Value of asset in 20 years@ 5.5% pa growth: $1.45m@ 8% pa growth: $2.33m

Note that the preceding table only includes the impact of income tax. It

Listen Now

Love PodBriefly?

If you like Podbriefly.com, please consider donating to support the ongoing development.

Support Us