Episode Details

Back to Episodes

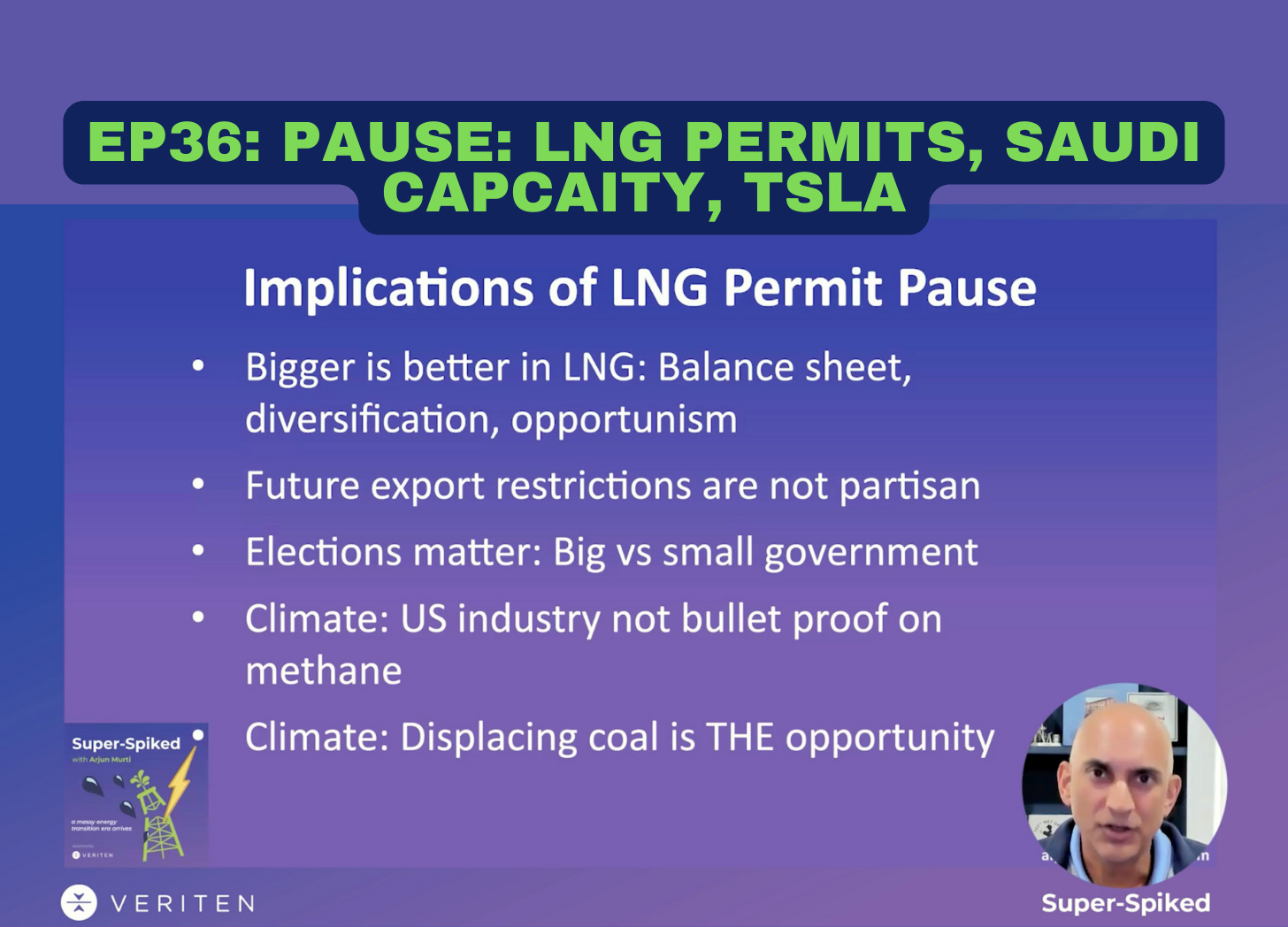

Super-Spiked Videopods (EP36): Pause: LNG Permits, Saudi Capacity, TSLA

Description

WATCH the video on YouTube by clicking the RED button above.

LISTEN to audio only via the Substack player by clicking the BLUEbutton above.

STREAM audio only on Apple Podcasts, Spotify, or your favorite podcast player app.

DOWNLOAD a pdf of the slide deck by clicking the blue Download button below.

We had intended to follow-up last weeks’ ROCE Deep Dive post (here) with examples of how to apply it to macro forecasting as well as sub-sector and company analysis. However, a surprise LNG permit “pause” from the Biden Administration followed a few days later by Saudi’s announcement it would “pause” its planned oil capacity expansion has led to a change in publishing plans!

We wrote a seven-part tweet/post on Twitter-X over the weekend (here) that has now garnered a mind-boggling 120,000 views, well above our typical 1,000-4,000 views per tweet/post. Key points: (1) there is no such thing as an “Industry” view on the “pause,” it essentially depends on whether a company, industry, or country is long or short natural gas; (2) the potential impact on Europe has been both over-analyzed and overstated; (3) the implications for developing Asia have been under-appreciated; (4) competitor countries are undoubtedly rejoicing over the news; (5) big versus small government is a basic viewpoint difference in how to address energy & environmental policy; (6) climate implications are more complex than the simple debate of LNG is higher-carbon than renewables versus lower carbon than coal.

We address the Saudi capacity expansion pause from the perspective of the recent Saudi oil policy that has focused primarily on the front-end of the curve. Is this a shift to focusing on long-dated oil? As a reminder, both the Biden LNG permit and Saudi capacity expansion pauses are consistent with our “Super Vol” rather than “super-cycle” commodity macro framework. Policy rhetoric and actions, frankly, can be as meaningful as underlying supply/demand, especially over the near-to-medium term.

Finally, we observe signs that we are past “peak Tesla,” especially when considered alongside clear evidence of electric vehicle (EV)-or-bust fatigue among car buyers and many traditional auto manufactures. China’s EV ramp continues, more or less unabated, and we believe is highly motivated by a desire to limit growth in oil imports. We do not believe there is a singular EV adoption “S-curve” for all regions. China will be different than the USA, which will be different than India, the rest of Southeast Asia, the Middle East, Africa, and Latin America. We continue to believe there is not a decade, let alone year, when we KNOW oil demand will peak, even as we expect continued growth in many new energy technologies including EVs.

🔔 4 Ways to Subscribe

* All Content: If you subscribe to Super-Spiked via email, you will receive all content to your inbox and it is also all on the Super-Spiked website. I have been aiming to publish about once a week, usually on Saturday.

Subscribe to Super-Spiked to receive all content via email and directly interact with me. Also available at https://veriten.com.

* Veriten: You can now also subscribe to Super-Spiked content via the Veriten website (here) and also receive Veriten’s flagship COBT video podcast.

* YouTube channel for video only: You can subscribe directly to the video feed of

Super-Spiked Videopods on my YouTube channel

Listen Now

Love PodBriefly?

If you like Podbriefly.com, please consider donating to support the ongoing development.

Support Us