Episode Details

Back to EpisodesTips on how to maximise your borrowing capacity

Description

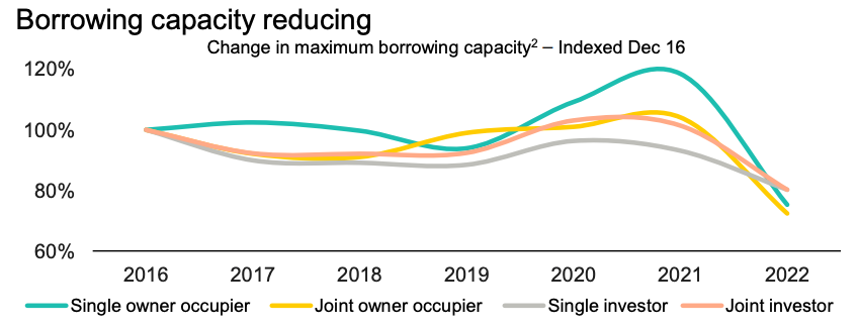

Borrowing capacity has reduced by around 30% over the past year due to the impact of higher interest rates and the increased 3% interest rate buffer that banks must use to calculate your borrowing capacity. This was eloquently depicted in this chart by CBA in February 2023.

{kind=link}

I wanted to explore the common strategies that people can use to safely maximise their borrowing capacity.

How to borrow safely

I’ve written several times that building wealth is a marathon not a sprint. Whilst it is good to avoid procrastinating and invest as much as possible, you should never take high risks.

When borrowing, it’s wise to plan for the worst but hope for the best. Look closely at your spending habits to ascertain how much you need to maintain a standard of living. Don’t rely (completely) on variable income such as bonuses. Test your ability to repay at higher interest rates – even if you think they are unlikely. And ensure you have adequate buffers in place to help you navigate any unforeseen changes in circumstances.

As a rule of thumb, if you are borrowing more than 6 to 8 times your total gross annual income, be careful. It could be a sign that you are borrowing too much. Consider the risks. You must have an exit strategy that you can implement if everything goes pear-shaped.

In my experience, it is unnecessary to borrow a huge amount to achieve your goals. People that do accumulate a lot of debt (i.e., what I would consider to be too much) usually do it because they are investing in the wrong properties. Property investing is a game of quality, not quantity. I would rather own one awesome, investment-grade property and have $1.5m of debt than a portfolio of 10 properties with $5.6 million of debt (I’m using an actual example of a portfolio that I saw recently). The former scenario will generate a lot higher risk-adjusted return over the next 20 to 30 years.

My overarching point is, be careful. Don’t overborrow.

Having said that, it is helpful to know what steps you can take to preserve and maximise your borrowing capacity. Here’s a few tips.

Consider using a charge card instead of a credit card

After many years (decades) of actively investing and using different banks, my wife and I ended up accumulating 7 credit cards! Notwithstanding that, they all charge an annual fee which is a waste of money, the aggregate credit limit was 6 figures!

Credit card limits reduce your borrowing capacity because the bank includes approximately 4% of the credit card limit as a monthly expense (to provide for a monthly repayment should you fully utilise the card/s). So, $100,000 of total credit card limits would result in a monthly expense of $4,000 in a banks serviceability calculation, thereby reducing your ability to borrow.

My wife and I always repaid our credit cards in full. We didn’t use them as a source of credit – merely to earn points. Therefore, a few years ago we cancelled all but one card (which we use for business expenses only) and obtained a charge card from American Express which we use for purchases, wherever possible. The advantage is that charge cards don’t have a credit limit because you must repay the full balance each month. So, they don’t impact your borrowing capacity.

Therefore, consider cancelling your credit cards to maximise your borrowing capacity.

If you earn variable income, be careful changing jobs

Many employees have a variable component as part of their overall remuneration package e.g., income that is contingent upon personal and/or company performance such as

My new book is available for pre-order now: Pre-ordering