Episode Details

Back to EpisodesWill Melbourne’s median house price exceed $2m by 2033?

Description

The unrefuted trend in all investment markets is mean reversion. It means that a period of below average returns is always followed by a period of above average returns. It is my thesis that investment-grade property in Melbourne looks attractive compared to other markets and that there are several economic tailwinds that may result in the median house prices doubling over the next decade.

The macro environment is positive for property

In short, property prices are driven by the law of supply and demand.

Demand for property is mainly dictated by interest rate settings, unemployment, and access to borrowings (mortgage lending).

Supply is mainly dictated by volume of new construction and consumer sentiment i.e., whether people are willing to buy and sell property. In times of higher uncertainty, most people stop transacting, as we’ve seen over the past 12 months.

Locking in higher discounts now will mean lower future interest rates

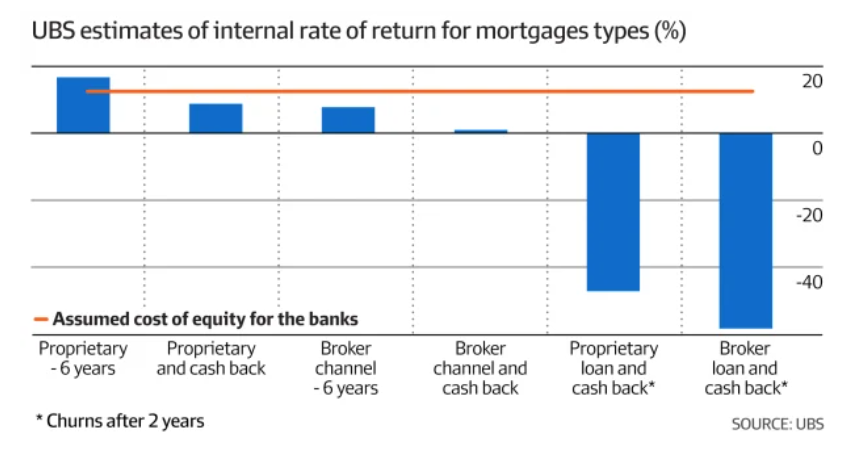

All the big 4 bank CEO’s have commented that the mortgage market has become the most competitive that it’s ever been in history. Banks are offering unusually high interest rate discounts and cash incentives to win and retain customers.

This chart (recently published in the AFR) suggests that banks are not generating a high enough return on new loans due to offering significant discounts. That means these discounts probably won’t last. I expect that banks will reduce discounting over the next 6 to 12 months once most of the low fixed rate loans have expired.

{kind=link}

As such, there’s a window of opportunity for investors to obtain an interest rate discount of 3% (or more) off the standard variable rate. Your discount will remain in place for the life of the loan.

The chart below sets out interest-only investment interest rates after applying a 3% discount since 2003 (when the data set began) i.e., back testing to see what impact a 3% discount would have had. The average interest rate would have been 4.2% p.a. over the past 20 years (of course, this is theoretical because you would have never received a discount of that size). I think it’s realistic to expect your average interest rate to range between 4% and 5% over the long run. You should do your calculations assuming 6% p.a., just to be safe.

CHART

We need more investors to solve the rental crisis

On average, borrowing capacity has reduced by around 30% over the past year due to (1) the RBA rate hikes and (2) APRA increasing the interest rate buffer that lenders use when testing your ability to repay a loan. This is depicted in the chart published by CBA in its results briefing in February 2023.

CHART

The rental crisis has been driven by a reduction in the number of properties that are available for rent, as I discussed here. There are fewer investment properties for two main reasons being (1) a lot of investors cashed in and sold during 2020 and 2021 and (2) tightening of lending rules since 2017.

The only way to solve the rental crisis is to increase the supply of privately owned rental properties, which is what the government will eventually have to do. They could achieve that by removing the interest rate premium that applies to investment loans (compared to home loans) and reducing the 3% interest rate serviceability buffer.

If/when they do that, it will increase investor demand which will stimulate the market.

High population growth and low unemployment is good for property

Australia’s unemployment rate is only 3.5% which is a historic low. The 10-year average unemployment rate is 5.4%,

My new book is available for pre-order now: Pre-ordering the